Log in as a...

New!

We’ve partnered with CREA to help improve your member experience and give your information the best security possible.

Click Here for additional instructions on the member login.

You will be returned to OREA once you have successfully logged in.

September 9th - 2013

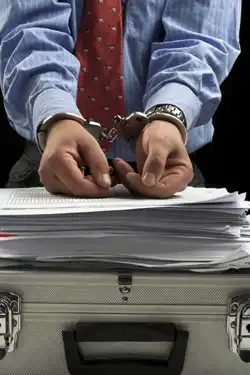

FINTRAC compliance: Know your responsibilities

Enduring a FINTRAC audit takes time and effort, but failure to comply can have serious consequences for you and your brokerage.

Enduring a FINTRAC audit takes time and effort, but failure to comply can have serious consequences for you and your brokerage.

Knowing your responsibilities under this legislation is vital. FINTRAC, which stands for the Financial Transactions and Reports Analysis Centre of Canada, was established to enforce the Proceeds of Crime (Money Laundering) and Terrorist Financing Act. The Canadian government introduced the act after the attacks of Sept. 11, 2001 in the U.S. The legislation was accompanied by new regulations requiring certain targeted “high-risk” industries, including real estate, to implement client identification and record keeping requirements.

The main requirements of the original legislation were to have a compliance program in place and to report suspicious and large cash transactions of $10,000 or more. The act came into force in 2000 and was expanded in 2001. Amendments to the act in 2008 created more obligations for various professions and industries, including real estate brokerages, brokers and salespersons.

As one REALTOR® learned recently, the process of responding to a FINTRAC audit involves specific and detailed expectations that can be time-consuming, particularly for a small brokerage.

Larry Maisonville heads a small brokerage in Queensville, Ontario. Since entering the real estate business 22 years ago, he has always been careful to dot his ‘i’s and cross his ‘t’s. He is a stickler for detail, and he feels that quality came in handy after he was selected for a FINTRAC audit – although he admits he was still nervous.

“It’s not enough to fill in some forms and forget about it,” says Maisonville. “If you’re a broker of record, don’t avoid thinking about FINTRAC. Don’t think it can’t happen to you, because that’s what I thought. You must examine what you’re doing and have a written program so that you’re prepared for an audit. Otherwise, it will keep you awake at night.”

A total of 1,126 businesses across the country were audited by FINTRAC in the past year, including real estate brokerages, banks, insurance companies and other sectors covered by the legislation. FINTRAC routinely selects brokerages from across the country for random audits to ensure that they are complying with the act. Written compliance and training programs are now required, along with risk assessments and a complete review of compliance measures every two years.

Although Maisonville was confident that he had complied with all of his FINTRAC obligations, he found the process of preparing the documents (namely the training, business assessment and reviews) difficult. He enlisted the help of a FINTRAC consultant to help with his compliance program, which he said was beneficial in identifying some gaps in his original program.

“The audit involves a significant amount of paperwork and the timelines are not necessarily flexible,” he says. “Everyone in your brokerage must understand the program to enable you to prepare for risks. How can you be sure that you know who your clients are?” As part of his audit requirements, Maisonville ended up compiling more than 100 pages of documentation.

A large brokerage has more staff to quickly pull together the necessary documents, but smaller shops may find the prospect of an audit overwhelming, he says. In a small brokerage where staffing is limited or non-existent, an audit can be an onerous task for even the most conscientious broker, he notes.

Maisonville felt intimidated when he first received notice about an audit. Consider the opening statement in the correspondence from FINTRAC: “This letter confirms that your organization has been selected from a compliance examination to verify its compliance with the requirements of Part 1 of the Proceeds of Crime (Money Laundering) and Terrorist Financing Act and its regulations.”

“Terrorist financing?! I was scared for a while,” Maisonville admits. “If my paperwork hadn’t been in order, I could have been facing some pretty stiff fines.” He advises other brokers to be acutely aware of their FINTRAC responsibilities and have written programs in place -- before the auditor comes calling.

Peter Lamey, the government spokesman for FINTRAC, says brokers must indeed take their financial responsibilities seriously. “We conduct exams to ensure that brokerages are complying with the act,” he says. “There have been monetary penalties in the past. When fines are issued, they tend to be proportional to the degree of non-compliance and the risk imposed on the system.”

Criminal penalties are another potential consequence for those who fail to comply, Lamey says. However, he notes that the FINTRAC requirements for accurate and thorough record-keeping serve a useful purpose under law. He points to a case in B.C., where FINTRAC documents led the police to arrest a man and issue a court order freezing $6 million of his real estate assets. In another case closer to home, a Hamilton brokerage was fined $27,000 for several violations, including: failure to appoint a person to be responsible for the implementation of a compliance program; failure to develop and apply written compliance policies and procedures that are kept up to date; and failure to assess and document risk.

“Record keeping obligations are now more extensive than they were before 2008,” Lamey says, although real estate professionals have been expected to comply since the act’s inception. The 2008 amendments ensure that FINTRAC is now in a better position to monitor requirements and assess whether brokerages are taking the necessary steps to meet their obligations, he says.

There are various reporting requirements for brokers under FINTRAC. Among them are responsibilities to:

- Report where there are reasonable grounds to suspect that a transaction or an attempted transaction is related to the commission or attempted commission of a money-laundering offence or a terrorist activity financing offence;

- Report where you know that there is property in your possession or control that is owned or controlled by or on behalf of a terrorist or a terrorist group;

- Report large cash transactions involving amounts of $10,000 or more received in cash.

Brokers must also keep the following records:

- Large cash transaction records

- Receipt of funds records

- Individual identification information records

- Corporate/entity identification information records

- Copies of suspicious transaction reports

Maisonville says most brokers know the basics of FINTRAC and its requirements, but the process of preparing all documents can be cumbersome on a tight deadline. A FINTRAC consultant helped him organize documents and develop an office manual. Other small brokerages may want to consider using a consultant as a way to save time and ensure the accuracy of the paperwork, he suggests.

“When you’re in business on your own, it’s a challenge,” he says. “You may be knowledgeable enough, but many of us in this line of work are too busy earning a living to have time for the level of administrative work involved.”

For more details about FINTRAC obligations, see FINTRAC Compliance in the OREApedia section of www.orea.com. See also the federal government’s FINTRAC website.

Share this item

For more information contact

Ontario Real Estate Association

Jean-Adrien Delicano

Manager, Media Relations

JeanAdrienD@orea.com

416-445-9910 ext. 246

Related Articles

Newsletter

Call for Candidates – Ontario Real Estate Association

October 31, 2022

Interested in running for a position on OREA’s 2023 Board of Directors?

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

October 31, 2022

Interested in running for a position on the Ontario REALTORS Care® Foundation’s 2023 Board of Directors?

Newsletter

Call for Candidates – Ontario Real Estate Association

November 26, 2021

Interested in running for a position on OREA’s 2022 Board of Directors? The following positions are up for election: two Directors-at-Large and four Provincial Directors (one each from the Southern, Northeastern, Western and Central Ontario Areas).

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

November 26, 2021

Interested in running for a position on the Ontario REALTORS Care® Foundation’s 2022 Board of Directors? The following positions are up for election: three REALTOR® Directors (made up of one each from the Central, Northeastern and Southern Ontario Areas), and one Public Director.

Newsletter

Call for Candidates – Ontario Real Estate Association

October 29, 2020

Interested in running for a position on OREA’s 2021 Board of Directors? The following positions are up for election: four Provincial Directors (made up of one each from the Central, Northern, Eastern and Western Ontario Areas) and two Directors-at-Large.

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

October 29, 2020

Interested in running for a position on the Ontario REALTORS Care® Foundation’s 2021 Board of Directors? The following positions are up for election: three REALTOR® Directors (made up of one each from the Northern, Eastern, and Western Ontario Areas), and one Public Director.

Newsletter

Call for Candidates – Ontario Real Estate Association

October 24, 2019

Interested in running for a position on OREA’s 2020 Board of Directors? The following positions are up for election: four Provincial Directors (made up of one each from the Central, Northern, Northeastern and Southern Ontario Areas) and two Directors-at-Large.

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

October 24, 2019

Interested in running for a position on the Ontario REALTORS Care® Foundation’s 2023 Board of Directors? The following positions are up for election: three REALTOR® Directors (made up of one each from the Eastern, Northern, and Western Ontario Areas), and one Public Director.

Newsletter

Call for Candidates – Ontario Real Estate Association

October 29, 2018

Interested in running for a position on OREA's 2019 Board of Directors? The following positions are up for election: four Provincial Directors (made up of one each from the Central, Eastern, Northern and Western Ontario Areas) and two Directors-at-large.

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

October 29, 2018

Interested in running for a position on the Ontario REALTORS Care® Foundation's 2019 Board of Directors? The following position are up for election: three REALTOR® Directors (made up of one each from the Eastern, Northern, and Western Ontario Areas), and on Public Director.

Newsletter

Call for Candidates – Ontario Real Estate Association (OREA)

November 15, 2017

Run for a position on OREA’s 2018 Board of Directors. The following positions are up for election: three Provincial Directors (made up of one each from the Southern, Northeastern and Central Ontario Areas), and two Directors-at-Large.

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

November 15, 2017

Run for a position on the Ontario REALTORS Care® Foundation’s 2018 Board of Directors? The following positions are up for election: three REALTOR® Directors (made up of one each from the Central, Southern, and Northeastern Ontario Areas), and one Public Director (Executive Officer).

Newsletter

Call for Candidates – Ontario Real Estate Association (OREA)

October 18, 2017

Run for a position on OREA’s 2018 Board of Directors. The following positions are up for election: three Provincial Directors (made up of one each from the Southern, Northeastern and Central Ontario Areas), and two Directors-at-Large.

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

October 18, 2017

Run for a position on the Ontario REALTORS Care® Foundation’s 2018 Board of Directors? The following positions are up for election: three REALTOR® Directors (made up of one each from the Central, Southern, and Northeastern Ontario Areas), and one Public Director (Executive Officer).

Newsletter

Working with seniors and boomers

June 23, 2017

Seniors and baby boomers are becoming a bigger segment of the population, and their real estate needs differ from those of other clients. Three Ontario REALTORS® discuss the joys and challenges of working with an aging demographic.

Newsletter

Co-operate, co-broker, communicate: Join seminar

June 19, 2017

Clarifying and documenting all of your communication with other REALTORS® is crucial when working on transactions that involve other brokerages. A web seminar (webinar) will explore this topic.

Newsletter

Venues announced for professional development events

June 19, 2017

Locations have now been confirmed for professional development and business strategy events in real estate this fall.

Newsletter

Provincial housing measures a success for REALTORS® and home buyers

June 19, 2017

The provincial government’s new plan to address housing challenges is the result of successful advocacy work by the Ontario Real Estate Association (OREA).

Newsletter

Three things REALTORS® should know about heritage properties

June 23, 2017

The township told the buyer that a rural property was safe to build on. A lawsuit ensued when the buyer later learned that a building permit was withheld because the land was located on a “no-build” buffer zone near a former dump site.

Newsletter

Legal Beat: Zoning confusion leads to lawsuit

June 24, 2017

The township told the buyer that a rural property was safe to build on. A lawsuit ensued when the buyer later learned that a building permit was withheld because the land was located on a “no-build” buffer zone near a former dump site.

Newsletter

Learn more about forms in upcoming seminars

June 19, 2017

Sign up for a web seminar (webinar) to learn more about the standard forms used in real estate transactions, and how they can help your trading activity.

Newsletter

Legal Forum reaches a milestone

June 19, 2017

Legal Forum, the popular online resource for Ontario REALTORS®, has answered its 6,000th question. This unique online service has been helping you for 17 years.

Newsletter

Support the motorcycle ride for charity

June 23, 2017

The Motorcycle Ride for Charity will take place on July 5. Join the ride or support a rider.

Newsletter

Real estate teams: Are they right for you?

May 24, 2017

Working as a part of a real estate team has pros and cons. Two Ontario REALTORS® discuss why it’s the right choice for them.

Newsletter

Seven tips to show your professionalism

May 24, 2017

Here are seven ways to demonstrate professionalism to real estate colleagues.

Newsletter

Master the offer process: Join seminar

May 24, 2017

Handling offers is an exciting but stressful part of real estate. Take part in a seminar to learn about different forms that can help you master the process.

Newsletter

Personal real estate corporations a step closer

May 24, 2017

Thanks to the success of recent advocacy work, Ontario Realtors are one step closer to being allowed to form personal real estate corporations.

Newsletter

Legal Beat: Make sure clients understand BRA before signing

May 24, 2017

The clients said they did not understand what they were signing when presented with a Buyer Representation Agreement. A judge offers advice to Realtors to prevent this all-too-common complaint.

Newsletter

New real estate app to develop business plan

May 24, 2017

An exciting and useful new app is now available for real estate professionals to develop a business plan and train for success.

Newsletter

Video tutorials explain forms

May 24, 2017

If you need help understanding and working with standard real estate forms, a short video tutorial can help.

Newsletter

College to stop delivery of real estate education

May 24, 2017

The OREA Real Estate College will no longer offer educational courses for real estate professionals in the province after December 31, 2020.

Newsletter

Supporters of charities, shelters honoured

May 24, 2017

Charity work by Ontario Realtors was the focus of a slate of awards presented recently by the Ontario REALTORS Care® Foundation.

Newsletter

Awards recognize leadership in real estate

May 24, 2017

Five REALTORS® were honoured at an awards luncheon as part of the Ontario Real Estate Association (OREA) annual conference recently.

Newsletter

Foundation board installed

May 24, 2017

The 2017 board of directors of the Ontario REALTORS Care® Foundation was officially installed at the annual OREA leadership conference in Toronto.

Newsletter

Time saving strategies for a busy spring

April 28, 2017

April showers typically bring an increase in business along with the May flowers. Don’t let the fast pace and increased demands of the busy spring season overwhelm you.

Newsletter

Nine ways to show your professionalism

April 28, 2017

Here are nine steps to demonstrate professionalism to your real estate colleagues.

Newsletter

Save the dates for professional development

April 28, 2017

Six events across the province can help you develop your skills and knowledge of real estate. Don’t miss Emerge: Moving You Forward with the Tools for Tomorrow.

Newsletter

Governance review explores OREA’s next chapter

April 28, 2017

Change is on the way for Ontario’s Realtors, as OREA and its members chart a new future for the association following Governance Day at the annual conference.

Newsletter

Legal Beat: Protect yourself, clients from illegal building

April 28, 2017

Realtors must disclose material facts about a property. Failure to verify the registration status of a newly built home can put you on the wrong end of a lawsuit.

Newsletter

Foundation gives over $1 million to charity

April 28, 2017

A new milestone has been reached, with more than $1 million given to charity by the Ontario REALTORS Care® Foundation last year.

Newsletter

New board of directors for 2017

April 28, 2017

The Ontario Real Estate Association officially installed its new president and board of directors at the recent annual general meeting and conference.

Newsletter

Get to know new OREA president

April 28, 2017

Ettore Cardarelli of Mississauga was installed as the new president of the Ontario Real Estate Association for 2017 at the annual OREA conference.

Newsletter

Tribute to outgoing president Ray Ferris at conference

April 28, 2017

The Ontario Real Estate Association paid tribute to outgoing president Ray Ferris at the annual general meeting in Toronto last month.

Newsletter

Greener fields? The challenges of rural real estate

March 23, 2017

Working in rural real estate does not always mean greener pastures. Three Ontario REALTORS® discuss the challenges of rural and recreational real estate.

Newsletter

Seven ways to handle stress

March 22, 2017

Real estate can be a stressful career. Here are seven tips to handle a stressful day.

Newsletter

Forms to help your daily trading: Join seminar

March 22, 2017

To learn more about the real estate forms that can help you in your day-to-day trading, sign up for an OREA web seminar (webinar).

Newsletter

RECO: Oral promise spurs complaint

March 22, 2017

The sellers of this house were told they would receive a rebate on terms and conditions, but that rebate never arrived.

Newsletter

Legal Beat: Dispute over nature of payment

March 22, 2017

The buyer could not come up with the deposit in this case, so the registrant put up her own money to keep the transaction alive. A dispute ensued when the deal fell apart.

Newsletter

Create home ownership affordability task force, OREA urges government

March 22, 2017

Representatives of the Ontario Real Estate Association (OREA) urge the government to set up a task force on affordable home ownership.

Newsletter

Learn more about forms in upcoming seminars

March 22, 2017

Sign up for a web seminar (webinar) to learn more about the standard forms and clauses used in real estate transactions.

Newsletter

OREA annual conference and governance day

March 22, 2017

The Ontario Real Estate Association annual conference begins on Feb. 27, and for the first time, it features a Governance Day.

Newsletter

Looking for committee volunteers

March 22, 2017

Volunteer for a committee as a way to serve your profession and enhance your knowledge and network.

Newsletter

Managing in the lean seasons

February 25, 2017

Winter is often a slow period in real estate. Three REALTORS® from different Ontario cities share their planning and budget strategies to survive the lean times.

Newsletter

Commercial real estate the focus of seminar

February 20, 2017

Learn more about your role and responsibilities in commercial transactions at an upcoming OREA web seminar.

Newsletter

Research guides decision making

February 25, 2017

Market and consumer research is crucial to success in real estate. Find out how OREA has enhanced its research capacity to serve you better.

Newsletter

Get help from Customer Service Centre

February 25, 2017

If you have questions or concerns about your real estate studies, the Customer Service Centre at the OREA Real Estate College can help.

Newsletter

That’s a RAP: New government relations initiative

February 25, 2017

The REALTOR® Advocacy Project (RAP) is a new initiative to ensure that your voice is heard loud and clear in government circles.

Newsletter

Legal Beat: Court dispute over unregistered trading

February 25, 2017

Advisory services were provided in this commercial case, and the company billed for its work, prompting a legal dispute over unregistered trading in real estate.

Newsletter

Learn more about forms in upcoming seminars

February 25, 2017

Sign up for a web seminar (webinar) to learn more about the standard forms and clauses used in real estate transactions.

Newsletter

Looking for volunteers

February 25, 2017

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

Save the date: OREA annual conference

February 25, 2017

The Ontario Real Estate Association’s annual assembly meeting and Ontario REALTORS Care® Foundation annual general meeting take place on March 1 in Toronto. These events are all part of the OREA 2017 Conference.

Newsletter

“Unreal” estate – Protecting buyers of unbuilt property

January 28, 2017

When buyers purchase an unbuilt property, common problems can arise. Three REALTORS® discuss ways to guide buyers through the pre-construction phase.

Newsletter

Positive response to ad campaign

January 28, 2017

A new phase of the ad campaign launched this past fall to promote the value of using a REALTOR® has had tremendous positive results, statistics reveal.

Newsletter

Nine things to do in real estate’s slow season

January 28, 2017

Don’t waste the quiet time. Use your days wisely this winter to prepare for the busy season.

Newsletter

Quiz: What kind of real estate athlete are you?

January 28, 2017

A fun and interactive quiz helps you figure out what kind of REALTOR® athlete you are.

Newsletter

New Year’s webinar: Updates on 2017 standard forms

January 28, 2017

Find out what’s new in real estate forms and clauses in 2017. Join OREA’s upcoming web seminar.

Newsletter

Save the dates: Upcoming webinars on standard forms

January 1, 2017

Nine webinars are being offered in 2017 to help you learn more about the standard forms and clauses used in real estate transactions.

Newsletter

Legal Beat: Contract may not be void if both sides treat it as valid

January 1, 2017

In this commercial case, a judge ruled that the parties had continued to act on the APS after the insurance clause date had expired.

Newsletter

Apply to win prestigious leadership award

January 2, 2017

If you’re new to real estate, involved in organized real estate or dedicated to community work, you can apply to win a prestigious award that helps you hone your leadership skills.

Newsletter

Looking for volunteers

January 3, 2017

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

First-time buyers get a tax break

January 4, 2017

Effective January 1, first-time home buyers will get a financial break on the purchase of their new home that is double the previous amount.

Newsletter

Political affairs conference a success

January 30, 2017

The political affairs conference held recently in Toronto was a great success, with the Ontario Real Estate Association event drawing members from across the province.

Newsletter

Call for Candidates – Ontario Real Estate Association

November 3, 2023

Interested in running for a position on OREA’s 2024 Board of Directors?

Newsletter

Call for Candidates – Ontario REALTORS Care® Foundation

November 3, 2023

Interested in running for a position on the Ontario REALTORS Care® Foundation’s 2024 Board of Directors?

Newsletter

Tough closings: Expect the unexpected

December 8, 2016

What should be the final, smooth step in a transaction can be fraught with complications. Three REALTORS® discuss closing problems and how to prevent them.

Newsletter

What’s new in real estate forms for 2017: Save the date

December 8, 2016

Find out what’s new in real estate forms and clauses in 2017. Join OREA’s upcoming web seminar.

Newsletter

Saying goodbye to your childhood home

December 8, 2016

The sale of the home in which you grew up can be an emotional experience. Editor Mary Ann Gratton discusses the impact of this milestone on herself and her family.

Newsletter

Call for candidates – OREA

December 8, 2016

Are you interested in running for a position on OREA’s board of directors? Find out more.

Newsletter

Call for candidates – Foundation

December 8, 2016

Are you interested in running for a position on the Ontario REALTORS Care® Foundation board of directors? Find out more.

Newsletter

Looking for volunteers

December 8, 2016

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

Apply to win prestigious leadership award

December 8, 2016

If you’re new to real estate, involved in organized real estate or dedicated to community work, you can apply to win a prestigious award that helps you hone your leadership skills.

Newsletter

Legal Beat – Size of deposit may affect forfeiture

December 8, 2016

In this commercial case, the buyers did not fulfill their side of the contract. The judge weighed in on whether the proposed penalty fit the damages suffered by the seller.

Newsletter

Save the date for OREA annual conference and AGM

December 8, 2016

The Ontario Real Estate Association’s Annual Assembly Meeting and REALTORS Care® Foundation Annual General Meeting take place on March 1 in Toronto. These events are all part of the OREA 2017 Conference.

Newsletter

Work-life balance in real estate

November 9, 2016

Finding time for your personal life can be a challenge in real estate. Three REALTORS® share their lessons for balancing work and personal time.

Newsletter

Residential leasing issues: Join seminar

November 9, 2016

Residential leasing is a specific type of real estate that can bring challenges involving landlords and tenants. Learn more at an upcoming web seminar.

Newsletter

The rise of heritage conservation districts

November 9, 2016

More than 22,000 heritage properties exist across the province today. Robert Hulley, an award-winning conservationist and former REALTOR®, explores the growth of this market niche.

Newsletter

Let’s talk about forms: OREA reaches out

November 9, 2016

The number and complexity of forms can be overwhelming in real estate. That’s why OREA launched the Forms Update Outreach Project. Learn more about this highly successful initiative.

Newsletter

RECO decision: Ad and listing agreement mislead sellers

November 9, 2016

A handwritten note to the sellers stated that if their property did not sell in 30 days, the brokerage would buy it at the highest price offered by the market. A registrant’s failure to properly document the details led to a RECO complaint.

Newsletter

Call for candidates – OREA

November 9, 2016

Are you interested in running for a position on OREA’s board of directors? Find out more.

Newsletter

Call for candidates – Foundation

November 9, 2016

Are you interested in running for a position on the Ontario REALTORS Care® Foundation board of directors? Find out more.

Newsletter

Legal Beat: Easement dispute prompts court cases

November 9, 2016

Access to a waterfront property became a point of dispute in this case. The issue hinged on whether the property required an easement of necessity.

Newsletter

OREA welcomes Tim Hudak as new CEO

November 9, 2016

After 21 years of distinguished public service in the Ontario legislature, Tim Hudak will join the Ontario Real Estate Association as Chief Executive Officer.

Newsletter

Ed Barisa retires as CEO of OREA

November 9, 2016

After 16 years as Chief Executive Officer of the Ontario Real Estate Association, Ed Barisa has announced his retirement.

Newsletter

In memoriam: Keith Teetzel

November 9, 2016

Keith Teetzel, a former long-time Executive Director of the Ontario Real Estate Association, died on Oct. 15.

Newsletter

Disclosure and stigmatized properties

October 19, 2016

Stigmatized properties present a special challenge in real estate, and REALTORS® should be aware of their disclosure obligations.

Newsletter

New ad campaign promotes REALTOR® value

October 19, 2016

An exciting new advertising campaign that promotes the value of using a REALTOR® to consumers was launched by the Ontario Real Estate Association.

Newsletter

Commercial real estate the focus of events

October 19, 2016

If you want to expand your knowledge of commercial real estate, come to one of two events organized as part of OREA’s fall Emerge lineup.

Newsletter

Legal Beat: Have a FINTRAC plan

October 19, 2016

Does your brokerage have a plan to prevent money laundering and other suspicious transactions? Make sure you comply with FINTRAC or face the consequences.

Newsletter

Maintain integrity with electronic signatures: Join seminar

October 19, 2016

Electronic signatures are being used more and more in real estate transactions. To maintain your integrity while using e-signatures, take part in an upcoming web seminar.

Newsletter

Fall events feature technology and strategy

October 19, 2016

This fall, come to one or more in a series of events designed to help you develop your skills and knowledge of real estate technology and strategy.

Newsletter

Generation Y’s intentions to buy real estate increase

October 19, 2016

More of Ontario’s younger generations are likely to buy a home in the next two years, according to new research from the Ontario Real Estate Association.

Newsletter

Motorcycle ride for charity a success

October 19, 2016

This year’s Motorcycle Ride for Charity was a great success, raising funds for a good cause. The annual ride supports shelter-based charities across the province.

Newsletter

RECO: Stigmatizing issues

October 19, 2016

There is nothing you can see, hear or measure that reveals a stigmatized property, but real estate professionals should understand the issues when representing consumers, says the Real Estate Council of Ontario (RECO).

Newsletter

Survivor: Real estate style

September 15, 2016

Don’t get voted off the island. To survive and thrive in real estate, you need a range of skills, according to three seasoned pros.

Newsletter

Need help with forms? See simple explanations

September 15, 2016

Forms are a key part of real estate, but they can be complex and full of baffling legal jargon. OREA’s Forms Explained is a resource that explains forms in plain English.

Newsletter

Campaign promotes REALTOR® value

September 15, 2016

The value of using a REALTOR® is the focus of a renewed advertising campaign set to launch this fall.

Newsletter

Topics and speakers announced for technology series

September 15, 2016

Topics and speakers for eight events have been confirmed as part of this fall’s series, Emerge: Moving You Forward with the Tools for Tomorrow.

Newsletter

Legal Beat: Tenant objects to candid camera

September 15, 2016

The landlord wanted to take photos of a rental unit in order to promote the space before selling it. The tenant objected, and a lawsuit ensued.

Newsletter

Consumer optimism grows over real estate markets

September 15, 2016

Ontarians are decidedly more upbeat about the province’s economy than they were last fall – a new and positive outlook that is boosting confidence, a new survey reveals.

Newsletter

RECO DECISION: Lot size error leads to complaint

September 15, 2016

After moving into their new property, the buyers discovered that the lot size was smaller than the measurements stated on the listing and marketing material.

Newsletter

Dealing with condominiums: Join seminar

September 15, 2016

Condominiums are a unique type of real estate. Learn more about the right forms and clauses used to address the specific challenges of condo purchases.

Newsletter

New and improved OREA blog

September 15, 2016

The Ontario Real Estate Association (OREA) blog has been redesigned and enhanced to meet your needs as a real estate professional.

Newsletter

Chattels versus fixtures: Explain the difference to clients

August 15, 2016

Ensure that your clients understand clearly which items will stay and which will go when a property sells. Three Realtors share insights.

Newsletter

Watch and learn: Tutorials explain forms

August 15, 2016

If you need help understanding and working with OREA Standard Forms, you can learn more from a new slate of tutorials. These online tutorials help you navigate the complexities of forms.

Newsletter

What does your OREA membership get you?

August 15, 2016

Find out what your association has been doing for you in the past year. Read the 2016 annual report from the Ontario Real Estate Association.

Newsletter

Consumer data can grow your real estate business

August 15, 2016

New and extensive research about consumers across the province can help you to grow your real estate business. These insights will greatly help you in understanding your local market.

Newsletter

Show integrity in real estate with the right forms: Join seminar

August 15, 2016

Integrity and professionalism are two key qualities that consumers want from REALTORS®. Learn more about using the right forms in real estate to maintain your integrity.

Newsletter

Legal beat: Life’s a beach for waterfront buyers

July 15, 2016

The buyers were attracted to a waterfront lot with access to a nearby beach. Wording in the real estate listing led to disciplinary action against two registrants.

Newsletter

Advocacy campaign wins second prestigious award

July 15, 2016

The Ontario Real Estate Association has won another prestigious public relations award for its advocacy campaign to stop the spread of the municipal land transfer tax beyond Toronto.

Newsletter

Venues announced for fall technology series

July 15, 2016

Location have now been confirmed for a series of technology and real estate business strategy events this fall.

Newsletter

RECO: Protect yourself against real estate fraud

July 15, 2016

Buying and selling real estate involves large monetary transactions. Protect yourself and your clients against different types of real estate fraud.

Newsletter

Emotions in real estate: Be a calming influence

June 17, 2016

Buying or selling a home is fraught with emotion. Three Ontario REALTORS® share their insights on steering clients through the emotional challenges of the transaction.

Newsletter

Kitec plumbing can cause problems

June 17, 2016

Kitec is a type of pipe that is vulnerable to premature failure, and REALTORS® should be aware of this product, which can lead to water damage and costly repairs.

Newsletter

Support the motorcycle ride for charity

June 17, 2016

Motorcycle season is upon us, and that means the Ontario REALTORS Care® Foundation is gearing up for a good cause. Join the 2016 ride or support a rider.

Newsletter

Do you have clause-trophobia? Join seminar

June 17, 2016

Writing clauses in real estate can be frustrating and stressful. Learn more about creating and using standard clauses by joining an upcoming web seminar at OREA.

Newsletter

Technology events enhance your skills

June 17, 2016

Dates are now confirmed for fall tools and technology events as part of Emerge: Moving You Forward with the Tools for Tomorrow. Find out about upcoming events in your region of the province.

Newsletter

Legal beat: A pool of problems for buyers

June 17, 2016

In this case, the swimming pool and equipment were said to be in good working order by the seller. The buyers’ failure to inspect the pool before closing meant that things did not go swimmingly.

Newsletter

Advocacy campaign wins prestigious award

June 17, 2016

A campaign organized by the Ontario Real Estate Association (OREA) to stop the spread of the municipal land transfer tax beyond Toronto has won a prestigious public relations award.

Newsletter

YPN awards recognize leadership in real estate

June 17, 2016

Five REALTORS® from across the province were honoured at an awards luncheon for their volunteer efforts and for supporting their communities.

Newsletter

Annual report highlights OREA accomplishments

June 17, 2016

Find out what your association has been doing for you in the past year. Read the 2016 annual report from the Ontario Real Estate Association.

Newsletter

Challenging clients: How to cope without losing your cool

May 8, 2016

To succeed in real estate, you must work with many personality types - some as different from you as night and day. Three Ontario REALTORS® talk about dealing with challenging clients.

Newsletter

What’s the big deal about real estate assignments? Join seminar

May 8, 2016

Assignment agreements have been the focus of much media attention recently. To learn more, take part an upcoming web seminar (webinar) offered by OREA.

Newsletter

The joys and challenges of working in real estate

May 8, 2016

Working in real estate can sometimes feel overwhelming, but there are joys as well as challenges. A REALTOR® from Pembroke, Ontario shares her views.

Newsletter

Legal beat: Get involved and stay involved

May 8, 2016

This lawsuit hinged on whether the registrant was sufficiently involved to earn a commission. The absence of a buyer representation agreement (BRA) may have sealed his fate.

Newsletter

OREA president featured on radio show

May 8, 2016

Ray Ferris, president of the Ontario Real Estate Association, is appearing as a guest expert on a popular radio series. He will discuss a range of real estate topics along with the value of using a REALTOR®.

Newsletter

Technology events enhance your skills

May 8, 2016

Dates are now confirmed for fall tools and technology events as part of Emerge: Moving You Forward with the Tools for Tomorrow. Find out about upcoming events in your region of the province.

Newsletter

Volunteers, milestones recognized at awards ceremony

May 8, 2016

Volunteers are the backbone of many organizations. That’s why the efforts of volunteers in the province’s real estate community were recognized by the Ontario Real Estate Association (OREA).

Newsletter

Supporters of charities, shelters recognized

May 8, 2016

Many REALTORS® help families find the perfect home, but they also do a great deal of volunteer work to support charities and shelters. The Ontario REALTORS Care® Foundation honoured various individuals for their charity work.

Newsletter

Foundation board of directors for 2016

May 8, 2016

The 2016 board of directors of the Ontario REALTORS Care® Foundation was officially installed at the annual general meeting in Toronto.

Newsletter

Let’s negotiate: Ability to reach agreement vital

April 18, 2016

If you lack negotiation skills, you won’t be able to put together a deal for your clients or stay in business for long. Three real estate professionals share their insights on negotiating.

Newsletter

New statistics and newsletter launched

April 18, 2016

A provincial statistics page and monthly newsletter from the Ontario Real Estate Association (OREA) are available with helpful market information.

Newsletter

Stickhandling offers and negotiations: Join seminar

April 18, 2016

The offer process is one of the most complex aspects of trading in real estate. To learn more, take part in the upcoming web seminar (webinar) offered by OREA.

Newsletter

Upcoming seminars on standard forms

April 18, 2016

More information about OREA standard forms is available through an ongoing seminar series. This spring, find out what’s coming in a series of web seminars (webinars) and sign up.

Newsletter

Real estate: More than just sales

April 18, 2016

The role of the REALTOR® is not so much salesperson as consultant, according to one Ontario real estate professional. In fact, selling is far from the whole picture, she argues.

Newsletter

New tutorials explain forms

April 18, 2016

If you need help understanding and working with OREA Standard Forms, you can learn more from a new slate of tutorials. Ten new online tutorials help you navigate the complexities of forms.

Newsletter

What a dump: Landfill discovered under dream home

April 18, 2016

The buyers learned belatedly that their dream home was built over a landfill site. Legal Beat discusses the court dispute over disclosure after a rural real estate sale.

Newsletter

What consumers need to know about assignments: RECO

April 18, 2016

Assignments in real estate have been the focus of media attention recently. The Real Estate Council of Ontario (RECO) answers questions about this type of transaction.

Newsletter

New OREA board of directors for 2016

April 18, 2016

The Ontario Real Estate Association officially installed its new president and board of directors at the annual general meeting in Toronto in March.

Newsletter

Time flies: Organizing your day

March 13, 2016

Staying organized and managing your workload effectively is vital to success in real estate. Three REALTORS® from across Ontario share their strategies for time management.

Newsletter

Changes to pre-registration education

March 13, 2016

Important changes are coming to pre-registration education on April 1 that will boost the knowledge of new entrants to the profession. The Real Estate Council of Ontario (RECO) is making changes with support from the Ontario Real Estate Association (OREA).

Newsletter

What’s new in Standard Forms: Join seminar

March 13, 2016

If you want to learn more about the standard forms used in real estate, sign up for a free seminar offered by the Ontario Real Estate Association.

Newsletter

New videos highlight consumer research findings

March 13, 2016

Two lively animated videos created by OREA reveal the results of surveys of consumers in the province of Ontario. They conclude with the importance of working with a REALTOR®.

Newsletter

Buyers floored by property’s structural weakness

March 13, 2016

A few years after purchasing a house, the buyers learned that previous owners had removed a load-bearing wall, rendering the second floor unsafe. The buyers sued the company that provided title insurance.

Newsletter

Last chance to volunteer for OREA committees

March 13, 2016

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

Local markets are stronger: Survey

March 13, 2016

Residential real estate markets are stronger now than they were a year ago, according to a recent survey of consumers. The Ontario Home Ownership Index, a survey conducted by OREA, reveals that 40 per cent felt the market in their own city was stronger in 2016.

Newsletter

Tips to protect your home and property: IBC

March 13, 2016

Review your home insurance policy and update your home inventory, advises the Insurance Bureau of Canada. These are among the steps you can take to protect your home and property, according to IBC.

Newsletter

Save the date: OREA annual conference and AGM

March 13, 2016

The Ontario Real Estate Association’s Annual Assembly Meeting and REALTORS Care Foundation Annual General Meeting take place on March 9 in Toronto. It’s all part of the OREA 2016 Leadership Conference.

Newsletter

Avoid errors in real estate listings

February 12, 2016

Mistakes in a real estate listing can hurt your clients and damage your career. That’s why accuracy in a listing is vital. Two experienced REALTORS® discuss common errors in listings and the consequences of making them.

Newsletter

Virtual home staging can save time, money

February 12, 2016

It’s now possible to stage a home without painting or decluttering, thanks to virtual home staging. Read the second of two stories on enhancing a property the digital way.

Newsletter

New seminars and tutorials deal with standard forms

February 12, 2016

Learn more about the forms often used in real estate by participating in an upcoming seminar or tutorial.

Newsletter

Customer Service Centre aims to help

February 12, 2016

If you have questions or concerns about your real estate studies, the Customer Service Centre at the OREA Real Estate College can help. The satisfaction rate among callers rose to 95%, up 3 percentage points.

Newsletter

Legal Beat: Faulty septic system makes for sale that stinks

February 12, 2016

This lawsuit hinged on the state of the septic system at a rural property and claims about plumbing expertise made by the registrant.

Newsletter

Videos focus on overcoming challenges, meeting goals

February 12, 2016

Learn how others have met challenges, surmounted obstacles or met their goals. Check out the Leadership podcasts posted to the Ontario Real Estate Association website.

Newsletter

Looking for committee volunteers

February 12, 2016

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

Save the date: OREA annual conference and AGM

February 12, 2016

The Ontario Real Estate Association’s Annual Assembly Meeting and REALTORS Care Foundation Annual General Meeting take place on March 9 in Toronto. These events are part of the OREA 2016 Leadership Conference.

Newsletter

Slowing down: Surviving the lean season

January 8, 2016

Winter is often one of the slowest periods in real estate, you must manage the slow times in order to remain in business during the hectic seasons. Three REALTORS® from different Ontario cities share their strategies for getting through the lean times.

Newsletter

Campaign prevents expanded land transfer tax

January 8, 2016

A high-profile advocacy campaign to prevent the spread of the hated municipal land transfer tax has been highly successful. The Ontario Real Estate Association was vigilant in lobbying Queen’s Park to ensure the MLTT does not extend beyond Toronto.

Newsletter

Living beyond your means in real estate

January 8, 2016

Avoid the temptation to spend too much or abuse your credit cards when you start to succeed in the business, advises a Toronto REALTOR®.

Newsletter

Apply to win a prestigious leadership award

January 8, 2016

If you’re new to real estate, involved in organized real estate and dedicated to doing community work, you can apply to win a prestigious award that helps you hone your leadership skills.

Newsletter

Home staging - the virtual way

January 8, 2016

If your clients don’t have the time or energy to declutter or repaint before listing their place for sale, you can suggest “virtual staging” to create a stylish picture that appeals to buyers.

Newsletter

Legal Beat: Alarm system leads to alarming lawsuit

January 8, 2016

The seller installed an alarm system in his home before putting it on the market. After the property sold, a dispute arose over the payment of monthly fees for the alarm monitoring service.

Newsletter

Looking for committee volunteers

January 8, 2016

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Volunteer for a committee as a way to serve your profession and enhance your knowledge.

Newsletter

Miss Real Estate Manners: Always be professional

January 8, 2016

Courtesy and professionalism are crucial in real estate. Read the final installment of tips in a series from the London and St. Thomas Association of REALTORS® (LSTAR).

Newsletter

Renovate before reselling? Some tips from RECO

January 8, 2016

If your clients plan to renovate before selling their home, they should remember that upgrades and repairs cost time and money. RECO provides tips to protect consumers and their pocketbooks.

Newsletter

Multiple offers pose unique challenges

December 22, 2015

A multiple offer situation requires attention to detail and due diligence on a number of fronts, no matter where the property is located. The EDGE newsletter spoke to three REALTORS® in different cities about how they handle competing offers.

Newsletter

What kind of REALTOR® superhero are you?

December 22, 2015

All REALTORS® are superheroes. Take part in a fun and interactive quiz to learn what kind of superhero you are.

Newsletter

Ontario government close to allowing doubling of land transfer taxes

December 22, 2015

The Ontario government has indicated it will make home buying even harder by giving all municipalities authority to levy a municipal land transfer tax (MLTT).

Newsletter

Call for candidates – OREA

December 22, 2015

Are you interested in running for a position on OREA’s board of directors? Find out more.

Newsletter

Call for Candidates – Foundation

December 22, 2015

Are you interested in running for a position on the Ontario REALTORS Care® Foundation board of directors? Find out more.

Newsletter

Get your home ready for winter: IBC

December 22, 2015

Short, dark days and colder temperatures are a reminder to start preparing your home for winter. The Insurance Bureau of Canada lists some steps to prepare for the arrival of those sub-zero days.

Newsletter

Legal Beat: Wet basement a reminder of buyer beware precedent

December 22, 2015

In this case, the buyers discovered a leak in the basement after moving into a house, and the concept of buyer beware played a key role in the court decision.

Newsletter

Miss Real Estate Manners: Protect your clients

December 22, 2015

Safety and compliance should be top of mind when you conduct a real estate showing. Read the latest installment of tips from the London and St. Thomas Association of REALTORS® (LSTAR).

Newsletter

Offer handling a common complaint: RECO

December 22, 2015

A high proportion of complaints to RECO pertain to the handling of offers. Make sure the process and your conduct are fair, ethical, open and transparent.

Newsletter

What kind of REALTOR® superhero are you?

November 23, 2015

The Ontario Real Estate Association (OREA) has developed a fun and interactive quiz that asks what kind of superhero you are. Play the game now.

Newsletter

Condo challenges: The particulars of the condominium market

November 23, 2015

Learn about the peculiarities of the condominium market from two REALTORS® who have been selling condos for 25 years or more. They share insights and experiences to help you navigate a market that is different from other residential real estate.

Newsletter

Romancing the real estate brokerage

November 23, 2015

Starting a career in real estate is like a new romance. Treat it like a budding romance to find yourself in wedded bliss rather than divorce court, advises one Ottawa Realtor.

Newsletter

Call for candidates – OREA

November 23, 2015

Are you interested in running for a position on OREA’s board of directors? Find out more.

Newsletter

Call for Candidates – Foundation

November 23, 2015

Are you interested in running for a position on the Ontario REALTORS Care® Foundation board of directors? Find out more.

Newsletter

Looking for volunteers on OREA committees

November 23, 2015

Joining a committee or task force is a great way to meet colleagues and contribute to the real estate profession. Serve your profession and enhance your knowledge by volunteering for a committee.

Newsletter

Legal Beat: Get your BRA signed

November 23, 2015

Getting a Buyer Representation Agreement (BRA) signed at the beginning would have prevented problems and a lawsuit in this commercial case.

Newsletter

Comic video highlights generation gap

November 23, 2015

A funny new video about a millennial client and her older REALTOR® exposes a generation gap in language.

Newsletter

Miss Real Estate Manners: Know your limits

November 23, 2015

Don’t overstep your bounds or give advice beyond your own level of expertise. Read the fifth installment of tips from the London and St. Thomas Association of REALTORS® (LSTAR).

Newsletter

Child's play: Working with young families

October 18, 2015

Showing properties is a crucial step in selling a home, but special challenges exist when young children are involved. Three REALTORS® talk about their approach to ensuring that everything runs smoothly.

Newsletter

REALTOR® value the focus of ad campaign

October 18, 2015

Television and billboard ads that promote the value of using a REALTOR® are running this fall across Ontario. The ads are part of the REALTORS® we do the homework campaign.

Newsletter

Don’t fear the heritage property

October 18, 2015

Heritage properties need not be a source of fear if you work in real estate. They are a substantial part of many markets across the province and one expert predicts their numbers will only increase over time.

Newsletter

RECO: Registrant fails to check zoning

October 18, 2015

The registrant in this transaction promoted a property as having two units, highlighting the rental potential with no mention of zoning restrictions. Read the decision from the Real Estate Council of Ontario after a complaint was submitted.

Newsletter

Technology events enhance your skills

October 18, 2015

Come to one or more events this fall to keep you on the cutting edge of technology in real estate and hone your skills. Sign up for an event as part of Emerge: Moving You Forward with the tools for Tomorrow.

Newsletter

Legal Beat: Brokerage sale leads to debate over turnkey operation

October 18, 2015

In this transaction, the owner sold her brokerage to buyers who later argued it was supposed to be a turnkey operation – a business already set up and ready to go with no changes needed. A lawsuit ensued.

Newsletter

Miss Real Estate Manners

October 18, 2015

Courtesy and common sense are vital ingredients for a successful real estate career. Read the fourth installment of tips and advice from the London and St. Thomas Association of REALTORS® (LSTAR).

Newsletter

Motorcycle ride a success

October 18, 2015

Sunny skies warmed the riders at this year’s Motorcycle Ride for Charity, who completed a successful ride from Toronto to Ottawa for a good cause. This year marked the 10th anniversary of the ride organized by the Ontario REALTORS Care® Foundation.

Newsletter

College wins prestigious award

October 18, 2015

The OREA Real Estate College has won a prestigious educational award for its blended learning curriculum from the Real Estate Educators Association, beating out hundreds of other programs across North America.

Newsletter

Mentorship in real estate

September 22, 2015

The guidance of experienced professionals can help you grow in your career and personal life. Mentorship takes different forms, from one-on-one sessions to group meetings or formal training. Three REALTORS® talk about how mentoring has helped them.

Newsletter

Complaints service helps at stressful time

September 22, 2015

It can be stressful to learn that you are the subject of a complaint to the Real Estate Council of Ontario. A service created by the Ontario Real Estate Association helps you navigate the process and know what to expect at a challenging time.

Newsletter

Serving buyers in the pre-construction phase

September 22, 2015

When a property is not yet built, ask many questions and use due diligence to prevent surprise and disappointment for your buyers, advises one Toronto REALTOR®.

Newsletter

Ad campaign promotes REALTOR® value

September 22, 2015

Television and billboard ads that promote the value of using a REALTOR® will be running this fall across the province. They are all part of the REALTORS® we do the homework campaign.

Newsletter

Video and webinar explain new form

September 22, 2015

A short video and web tutorial help you understand Form 801, the new document created to help comply with legislation to prevent phantom offers.

Newsletter

Fall technology events

September 22, 2015

Dates and locations are now confirmed for fall tools and technology events as part of Emerge: Moving You Forward with the Tools for Tomorrow. Find out about upcoming events in your region of the province.

Newsletter

Legal Beat: When you don’t have a crystal ball

September 22, 2015

The seller took legal action against her REALTOR®, claiming she was misled by flawed advice to sell her property at a price below market value.

Newsletter

Consumer confidence in local markets growing

September 22, 2015

More Ontarians have a favourable opinion of the real estate market in their local city or town, according to new research released in an index produced by the Ontario Real Estate Association.

Newsletter

Miss Real Estate Manners

September 22, 2015

Courtesy is paramount in the real estate industry, according to the latest installment of tips and advice on professional behaviour in real estate from the London and St. Thomas Association of REALTORS®.

Newsletter

Handling stress in real estate

August 22, 2015

Real estate can be a stressful career. Erratic hours, stiff competition and an uncertain income all contribute to the stress. Three seasoned REALTORS® talk about how they cope with stress and share their tips.

Newsletter

Electronic signatures now allowed for agreement of purchase and sale

July 1, 2015

Legislation is now in place to allow electronic signatures to be used for the agreement of purchase and sale (APS) in real estate transactions.

Newsletter

New form deals with law to prevent phantom offers

August 22, 2015

A new form is available to help you comply with legislation aimed at preventing phantom offers. The Ontario Real Estate Association has created Form 801, an offer summary document that satisfies the conditions of Bill 55, The Stronger Protection for Consumers Act.

Newsletter

RECO: Registrant switches brokerages and changes lawn signs

August 22, 2015

The registrant moved to a new brokerage and changed the lawn signs on properties for clients whom he had represented through his old brokerage. Read the decision from the Real Estate Council of Ontario after complaints were submitted.

Newsletter

Get organized and stay organized

August 22, 2015

Managing your time in the demanding real estate profession can be a challenge. REALTOR® Eric McCartney of York Region shares some of his insights into getting – and staying – organized.

Newsletter

Fall into technology events

July 18, 2015

If you want to stay on the cutting edge of technology in real estate, come to one or more events this fall around the province as part of the series called Emerge: Moving You Forward with the Tools for Tomorrow.

Newsletter

Consumers show confidence in local markets: Index

July 18, 2015

What do Ontario consumers really think about the current real estate market? Learn more in the newest results from the Ontario Home Ownership Index research study.

Newsletter

Legal Beat: Lack of electricity a reminder that REALTORS® must verify facts

July 18, 2015

The registrant was selling two vacant rural lots and his signs and advertisements stated that the properties were “fully serviced” by an electricity source on the road at the edge of the property. A court case ensued when the buyer learned that electricity service was lacking.

Newsletter

Miss Real Estate Manners: Do unto others

July 18, 2015

Treat your colleagues, customers and clients the way you would like to be treated. Read the second installment of tips and advice from the London and St. Thomas Association of REALTORS® (LSTAR).

Newsletter

Miss Real Estate Manners: Show courtesy

June 7, 2015

Courtesy, communication and common sense are the three “C”s that real estate brokers and salespeople should follow in doing business. The London and St. Thomas Association of REALTORS® shares some tips from its “Miss Real Estate Manners” summary of good behaviour.

Newsletter

Motorcycle ride for charity celebrates 10th anniversary

June 5, 2015

The rubber meets the road on Wednesday, July 8 in this year’s Motorcycle Ride for Charity. Take part in the ride or sponsor a rider to support the many shelter-related charities that benefit from the ride organized by the Ontario REALTORS Care® Foundation.

Newsletter

Avoid advertising pitfalls

June 8, 2015

Make sure your real estate advertisements follow the provincial guidelines to prevent complaints and fines for false or misleading advertising. The industry regulator, the Real Estate Council of Ontario, outlines some of the most common mistakes spotted in real estate ads.

Newsletter

Wired Office: Big data is key to real estate service

June 6, 2015

Big data is everywhere, and more consumers are doing at least some online searches of their own before contacting a REALTOR®. Find out how big data can help you give a better service to your clients and customers even in today’s wired world.

Newsletter

Legal Beat: Buyers will find out eventually

June 4, 2015

The sellers in this case experienced water damage at their property, a fact not disclosed during the real estate transaction. A lawsuit was launched after the buyers learned from their new neighbours about previous water and mould problems at the house.

Newsletter

Awards honour volunteers, milestones

June 3, 2015

Volunteers are the backbone of many organizations. That’s why the efforts of volunteers in the province’s real estate community were recognized by the Ontario Real Estate Association (OREA).

Newsletter

OREA training video popular

June 1, 2015

A video blog post on how to give clear classroom instructions has found popularity on YouTube. It is just one in a series of instructional videos for trainers that help facilitate classroom sessions.

Newsletter

Supporters of charities, shelters recognized

June 2, 2015

Many REALTORS® help families find the perfect home, but they also do a great deal of volunteer work to support charities that give shelter to the homeless and others in need. The Ontario REALTORS Care® Foundation honoured various individuals and groups for their charity work.

Newsletter

Four tips for a hassle-free move: RECO

June 8, 2015

The Real Estate Council of Ontario (RECO) has published tips to help consumers select the best mover. Share these tips from Consumer Protection Ontario with your clients and customers.

Newsletter

Hone your negotiation skills

May 6, 2015

Even a flock of chickens can be the subject of dispute in a real estate transaction. Negotiation is vital in this line of work, and the more you hone your negotiating skills, the more successful your career will be. Read more about negotiating skills and the art of the deal from three Ontario REALTORS®.

Newsletter

Developing your brand

May 5, 2015

Branding in real estate yields tangible results. A pair of REALTORS® learned this after asking some tough questions in the process of developing their brand. Find out how an Ottawa team achieved lasting recognition by developing its brand.

Newsletter

Rules vary for basement apartments, second suites

May 5, 2015

Be cautious in your approach to properties with basement apartments, second suites or in-law suites. That’s because the laws vary across the province and can be a legal minefield.

Newsletter

President’s Message from Patricia Verge

May 4, 2015

The president of the Ontario Real Estate Association notes that change is the new normal in today’s business world. Patricia Verge discusses the challenges and changes in real estate today.

Newsletter

RECO decision: Memory fails registrant who conveys wrong price

May 5, 2015

A registrant’s mistaken price presentation leaves the sellers out of pocket and the buyers out of luck following this transaction, which leads to a RECO complaint.

Newsletter

Legal Beat: Saturday closing leads to lawsuit

May 2, 2015

A closing that was scheduled for a Saturday in an agreement of purchase and sale (APS) led to legal issues in an Ontario property transaction.

Newsletter

Unveiling the OREA Real Estate College alumni program

May 6, 2015

A graduate’s connection to his or her college should not end on graduation. That’s why the OREA Real Estate College has launched a new alumni program.

Newsletter

Snapshot of OREA members revealed

May 3, 2015

A new survey of members of the Ontario Real Estate Association (OREA) provides valuable information and helps create a profile of members across the province. Find out more about the age, language, locations, and type of real estate transactions conducted by members.

Newsletter

Motorcycle ride for charity

May 2, 2015

This year’s Motorcycle Ride for Charity organized by the Ontario REALTORS Care® Foundation will take place on Wednesday, July 8. Riders depart from the OREA headquarters in Don Mills, with several stops on the way to Ottawa.

Newsletter

Annual report now available

May 1, 2015

An interactive version of the 2015 annual report of the Ontario Real Estate Association is now posted to the OREA website, with electronic links to bring you more information on the products and services provided by OREA.

Newsletter

Bridging the generation gap in real estate

May 3, 2015

It has never been more important for young and old to work together. In an industry that is constantly evolving, both new and seasoned REALTORS® must collaborate and share knowledge, argues one Ontario broker.

Newsletter

Foundation board installed

May 1, 2015

The board of directors of the Ontario REALTORS Care® Foundation for 2015 was officially installed at the annual OREA conference.

Newsletter

RECO website refreshed

May 3, 2015

The Real Estate Council of Ontario recently unveiled its new website. The site has been revised to better serve the needs of both consumers and real estate professionals.

Newsletter

The importance of repeat business and referrals

April 4, 2015

Word-of-mouth advertising is a vital way to build your business. Referrals and repeat business are crucial to your success in real estate. In this feature article, three Ontario REALTORS® talk about the strategies they use to get referrals and generate repeat business.

Newsletter

REALTOR® value advertising campaign continues

April 3, 2015

An ad campaign designed to promote REALTOR® value to the public will continue until the end of 2018. That decision is the result of a vote on a special levy to fund the extension of the campaign at the annual general meeting of the Ontario Real Estate Association (OREA).

Newsletter

The benefits of volunteering in real estate

April 1, 2015

Many personal and professional benefits come from volunteering, as the president of a local real estate association learned after a year in office.

Newsletter

REALTOR® Quest the largest show of its kind

April 2, 2015

On May 6 and 7, thousands of real estate professionals will gather at the Toronto Congress Centre for Canada’s largest REALTOR® trade show and conference, featuring seminars, learning opportunities and up to 240 exhibitors.

Newsletter

Personal real estate corporations the focus of bill

April 3, 2015

A bill introduced recently at Queen’s Park aims to change legislation to allow real estate salespeople in Ontario to incorporate. The Tax Fairness for Realtors Act would bring Ontario in line with six other Canadian provinces.

Newsletter

Legal Beat: Use forms properly and fill in the blanks

April 2, 2015

A contract became null and void after forms were not completed properly and a notice waiving conditions was not delivered personally to the seller.

Newsletter

Technology and real estate the focus of event

April 3, 2015

RETechTalks is a conference with a focus on technology and real estate, described as a day to learn from the very best people in Toronto real estate.

Newsletter

OREA News: New board of directors for 2015

April 3, 2015

The Ontario Real Estate Association officially installed its new president and board of directors at the annual meeting in Toronto on March 11.

Newsletter

Market Watch: Housing affordability slips nationally

April 1, 2015

Solid increases in Ontario home prices were key to the slight erosion in housing affordability across Canada, according to a housing trends report.

Newsletter

Surviving the busy spring season

March 26, 2015

Although springtime means sunshine and flowers in bloom, it represents the busiest time of year in real estate. Three experienced Ontario REALTORS® share their ideas and insights on how to cope and thrive during the industry’s busiest season.

Newsletter

Green real estate conference

March 19, 2015

The business case for environment-friendly buildings has never been stronger. Learn more at the upcoming Green Real Estate Conference on April 23 at the Metro Toronto Convention Centre.

Newsletter

Women’s hockey star and IBC promote road safety

March 19, 2015

Drive according to weather conditions. That’s the message of a new road safety video produced by the Insurance Bureau of Canada (IBC) featuring Canadian women’s hockey star Kelly Terry. Watch the video here.

Newsletter

RECO: Agreement to lease doesn’t show that tenant would rent to students

March 22, 2015

In this RECO decision, the registrant was disciplined after the owner of a property discovered that her property had been turned into a rooming house for students.

Newsletter

Remind consumers to hire contractors who work safely

March 24, 2015

Renovation work done by the wrong contractor can create expensive problems. The Ontario Ministry of Government and Consumer Services has crafted tips to help consumers select contractors who work safely.

Newsletter

Legal Beat: Installation of ATM the focus of commercial dispute

March 25, 2015

The landlord and tenant in this commercial dispute disagreed over the installation of an automated teller machine (ATM) on the property. The court case drained cash at a pace that rivalled that of the dispensing machine itself.

Newsletter

New advertisements released in REALTOR® value campaign

March 20, 2015

An exciting new slate of advertisements is being released March 2 to promote REALTOR® value to consumers across Ontario.

Newsletter

OREA website refreshed

March 20, 2015

A bold new look and feel is evident on the OREA website, making it quicker and easier for you to get what you need to succeed in your real estate career.

Newsletter

News: Call for volunteers

March 20, 2015

Joining a committee or task force is a great way to meet real estate colleagues and make a contribution to your profession. The deadline to apply is March 20.

Newsletter

Welcome to the digital EDGE

February 22, 2015

OREA is pleased to launch an all-electronic version of The REALTOR® EDGE newsletter, full of useful news and information to help you in your real estate business.

Newsletter

Safety first should be motto for REALTORS®

February 22, 2015

Safety is highly important for those working in real estate. Three REALTORS® share their experiences and talk about the importance of taking precautions when showing properties or hosting an open house.

Newsletter

Broader export demand predicted: RBC

February 22, 2015

Canada’s economy is expected to see higher export growth in 2015, despite the recent decline of oil prices, says a new report.

Newsletter

Housing outlook for 2015 shows modest gains

February 22, 2015

Most regions posted modest gains in average prices of residential homes despite increased inventory in many of Canada’s housing markets, according to a recent report from RE/MAX.

Newsletter

Levy recommended to fund REALTOR® value ad campaign

February 22, 2015

For two years OREA has promoted the value of REALTORS® via a mass advertising campaign. Delegates to the OREA AGM in March will be asked to vote on a special levy to continue to fund the campaign.

Newsletter

Ontarians feel better about economy, real estate markets

February 22, 2015

Six out of 10 Ontarians surveyed say the state of their city’s economy is good, up from 53 per cent last year, according to a research study commissioned by OREA and Ipsos Reid.

Newsletter

Embracing the growing heritage market

February 22, 2015

The heritage market is growing swiftly thanks to a boom in home renovations. Conservation expert Robert Hulley shares his insights for REALTORS® who want to capitalize on the opportunities.

Newsletter

Legal Beat: Plaintiff in commercial case has great expectations

February 22, 2015

An executive seeking to develop commercial condos spent nearly $100,000 on marketing then sued his brokerage for reimbursement after the relationship soured.

Newsletter

Save the date

February 22, 2015